Did you know, that for every $100,000 of loan you take out, your annual payment will be roughly $6,000. Whoa there! How did I know that?

If you haven’t read this article yet, it gives good tips on how you can calculate an annual loan payment quickly using a rule of thumb. It basically says that for a 30 year loan at about 4% interest, you can expect your annual loan repayment to be $6,000. It’s actually $5,724 but you wouldn’t know that without using a mortgage calculator.

If you don’t have access to a mortgage calculator, then keep this simple rule in mind: roughly 6% of the loan is your annual loan repayment amount. This means 4% is interest and roughly the remaining 2% is principal.

In today’s article we are going to show you how to apply this mental math rule in helping you quickly calculate how much house you can afford without having access to a calculator.

You’ll need to know your income of course and you need to know how much of your income you are willing to dedicate to paying for a mortgage.

Most financial advisers would recommend spending no more than 25% of your take home income on your mortgage payment. Dave Ramsey would say no more than 25% on your total housing debt budget. This includes property taxes and property insurance, and for some people it includes property mortgage insurance (PMI).

Banks and lenders may recommend no more than 35% of pre-tax income.

For purpose of the quick rule today, we will use 25% of your take home income as our rule for maximum that should be spent on your principal and interest mortgage payment. It doesn’t include property taxes and insurance. If you want a rule for maximum total debt payment that included taxes & insurance on top of the loan repayment, then use 33%.

Let’s get to the math now.

Say, for example, your take home pay is $48,000 (meaning you’ve already had taxes withheld). Using our 25% rule for maximum loan amount, you can afford a house that has an annual payment of $12,000.

$48,000 x 25% of take home pay = $12,000 of income spent on mortgage payment.This leaves you $36,000 to cover other cost of living expenses and money you can save or invest towards retirement.

Now that you know how much you can spend a year on the principal and interest mortgage payment combined, use the $6,000 payment per $100,000 loan rule to calculate how much house you can afford.

In this example, you could afford a $200,000 loan.

Assuming you put down 20% and took out a loan for 80%, you could afford $250,000 of house. You would put down $50,000 (20%) and take out a $200,000 loan (80%). Your $200,000 loan at a fixed rate of 4% over 30 years would cost you roughly $12,000 in repayment each year. $12,000 is 25% of your take home pay of $48,000, putting you in the green light for affordability based on your income.

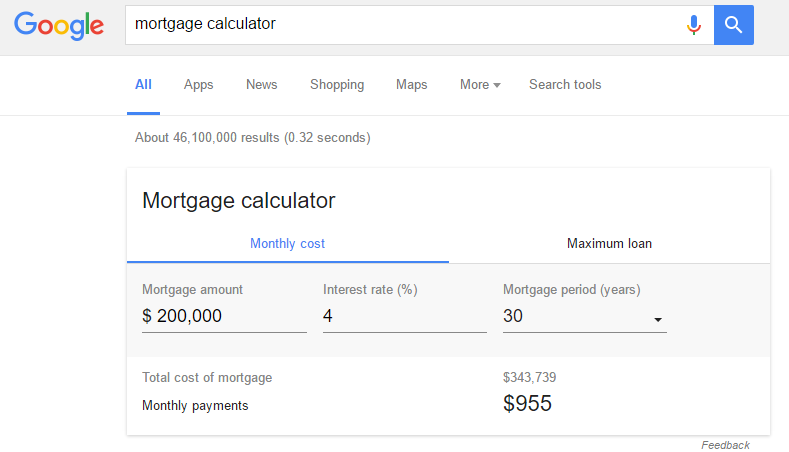

Here is a photo of the mortgage calculator on Google confirming that this rule of thumb is close to the actual results. Our $12,000 per year rule of thumb would be about $1,000 per month you’d pay.

It takes a little mental math and working backwards but it will be a fairly quick way of estimating how much home you can afford without having access to a mortgage calculator.

Method #2: Multiply Your Take Home Pay

Super Quick Rule: Multiply your take home pay by 4 to calculate a conservatively affordable loan amount and then determine the down payment you’d make and add it onto the loan amount to calculate the total house value.

Take Home Pay: $50,000 x 4 (Rule of Thumb) = $200,000 loan that is affordable based on my income.

Total House Value You Can Afford: $200,000 (80%) + $50,000 (20% down payment) = $250,000

There you have it, two different methods to calculate house affordability. One takes more mental math and working backwards. The other method you simply multiply your take home pay by 4 and then add on the down payment.

Here is an affordability calculator if you want to accurately determine how much debt you can afford to take on when looking to purchase a home.

If you’d like to search for a home for sale in Elkhart, Indiana and the surrounding area, I’d be happy to work with you and help you make a seamless transition to your new home. Contact me via one of these methods:

- Phone 574-536-9218

- Email: Nick@TeamFoy.com

- Or by filling out this contact form

Looking forward to assisting you,

Kevin Foy, Elkhart Real Estate Agent

P.S. Keep up to date with the latest news in Elkhart, Indiana by following my Facebook page here.